Recently, Mrs Budget and I have been talking about our future kids. That’s because people around us are either married with kids or are actively making plans to have their kids soon.

Of course, for Mrs Budget and myself, we are thinking of trying to conceive only 1 or 2 years down the road, or at least 1 or 2 years after we get married.

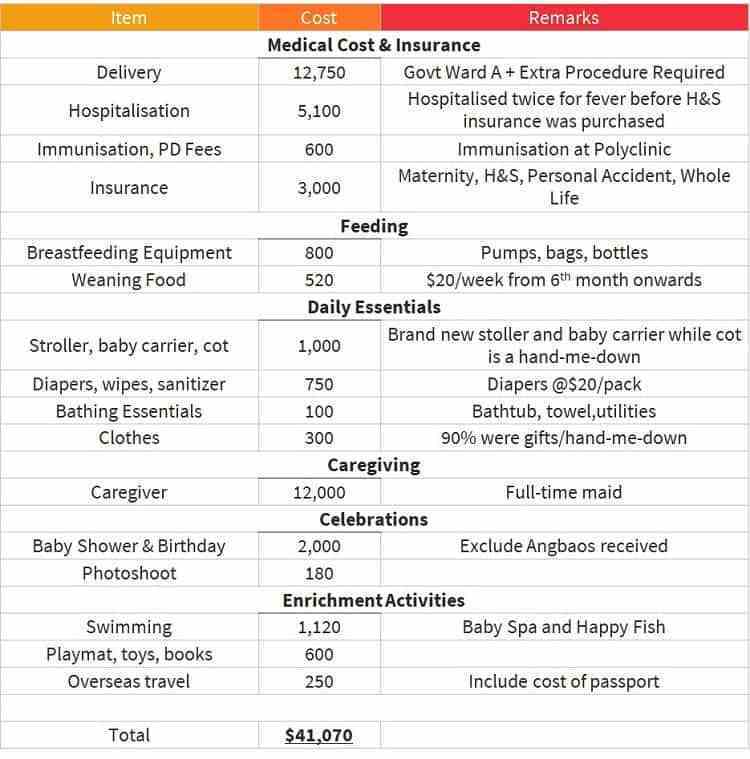

Mr Budget chanced upon a recent article by Heartland Boy where he detailed the cost of his first born, and the figure actually raised a few reasons for concern for us.

According to his calculation, the total cost of raising his first born amounted to approximately S$41,000. Here’s the calculation by Heartland Boy (all credits belong to Heartland Boy)

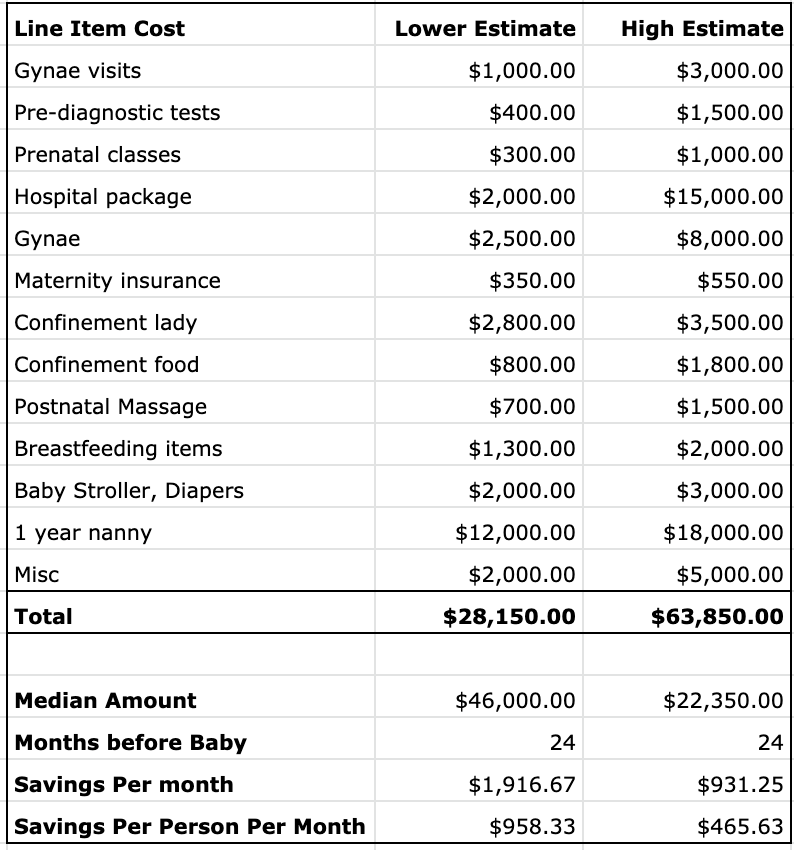

S$41,000 seems like a lot of money and hence, we decided to do some budgeting on our side. To do that, we compare Heartland Boy’s figure as well as SG Budget Babe’s figure to come out with a median amount of what we need to budget for our first child.

Here’s our budgeting table:

What we did was to get the various line items and tabulate it. While SG Budget Babe suggested a budget of S$30,000, Heartland Boy end up spending S$41,000.

If we took the median amount between the low and high estimate, we will come out with a budget of S$46,000. Dividing that with 24 months to save for the money required, the savings per month required is S$1,916.67. This is quite a huge amount to save up every month!

Of course, we ask ourselves, spending S$46,000 is a bit of a luxury, and knowing Mrs Budget and myself, we will try to avoid unnecessary luxury.

So, if we were to remove some optional items from the lower estimate figures (prenatal classes, confinement food, misc items), the amount that we need to save up turns out to be S$22,350, a much more palatable budget.

Of course, even if it is at S$22,350, the savings per month required is still at S$931.25, or at S$465.63 per person.

For Mrs Budget and myself, we will most likely be using that as a guideline and be setting aside a baby fund for that. Of course, we do have our current savings now that we can use as our baby fund, and we will have to discuss how we want to do this.

Sometimes I feel like we might be overthinking all these budgeting – because if we have a high savings rate, our monthly bank balance will increase, and indirectly, our baby fund will come from our monthly savings, and we don’t have to overthink it.

So the question really is, is it better to start a separate regular savings plan for 12 – 24 months to be used as our baby fund, with us contributing S$500 monthly each?

Or is it better to just keep everything business as usual, and when the baby comes, we will drawdown from our individual bank accounts? After all, if we have a high cash in hand (baby fund + current bank balance), we can enjoy a higher interest rate from our current high yield account?

Will be good to hear from young couples with prior experiences. 🙂

Also, a very warm welcome to our new followers: Charlotterria, Mugilan, Chelsea, Nelson, Jonnypalive, Aileen. Thanks for the email follow. 🙂

Like our Facebook Page for more articles like this: Mr Mrs Budget

I think a budget of 22k is probably too tight if you are going for private hospital Single bed room package. 30k should be a comfortable sum. The avg cost of delivery in private hospital is about 20k, not withstanding the medisave claim of about 4-5k. For necessities like baby cot, breast pumps, diapers, clothes and towels, I spent around 1.5k with no hand-me-down.

LikeLike

Hi Wei Long,

Thanks for sharing your experiences. We are thinking of going with public holiday / KKH instead of a private one. Mrs Budget insisted on that too. So I think we will be working on a S$20k -S$25k budget.

Did you set aside a baby fund into a separate account or did you drawdown the S$20k from your savings account? 🙂

LikeLike

I see. KKH private class A ward charges is similar to TMC. Unless your wife’s company has subsidy for govt hospital delivery.

Hmmm nope I dun have a baby fund, but I made sure to have at least 20k in my bank at all times. For me delivery charges is manageable because you are paying at stages and via credit cards. For confinement nanny is straight cash, so that amount has to be set aside.

LikeLike

Hi Wei Long,

yeaps – same as you, it looks like we will most likely not have a baby fund, but mentally earmark a small budget from our bank accounts for when we are ready to have our kid soon. 🙂 $20k seems like a safe amount!

LikeLike

Yup. Each couple has their own financial style. So find one that is comfortable with both of u. Saw that your annual div is ard 3k. Meanwhile can continue to grow your div. This will help to offset some of the associated costs. It definitely helps for my case. At least my cash flow is not that tight because I know I have my monthly div to fall back on.

LikeLike

Personally I think $20k cash on hand is more than enough.

Me and wife both PR. We did our gynae visit as class C in KK hospital and only convert to Class A in 3rd trimester. After born baby stayed in special nursery unit for 2 days. Separate admission of 9 days (class C because no different from class A) after discharge. Hired confinement lady from Msia.

Total cash damage around $10k with the rest from Medisave.

LikeLike

Hi Anon!

Oo S$10k sounds like a much more affordable figure to work with. For the confinement lady from Msia, is it that your kid are staying in Msia? Im from Malaysia too!

LikeLike

Father of a 6mth old baby here. There is quite abit of financial assistance. 8K in baby bonus, medisave for delivery and also 900 claimable for your gyne visits.

I did not spend any out of pocket delivering in Mt A via normal delivery in a 2 bedder ward. Still have 500 bucks spare after all payment from the first trench of 3K in baby bonus

LikeLike

Hi F2! Thanks for sharing! I’ve got to check on the baby bonuses! Yeah at the back of my mind, i feel like the figures i presented might be on the high side and anything above S$30,000 is a bit too luxurious.

LikeLike

Father of a soon to be 6 year old.

Prepare baby fund like rich dad purchase his wants. Buy asset to generate income that buy his car.

So buy income generating asset whose income will be paying your baby costs. It will be a huge help. And yes I also believe it to be best to delay kids until u haf make your financial foundation stable. Significant income coming in not from yur salaries. Savings get burned. Stable assets should maintain providing u income consistently.

And I believe u r on the right track when u are able to remove the wants and reduce yur budget to 20k.

I believe expense would not increase uncontrollably unless unfortunate circumstance occur like hospitalisation or using private hospital. Hell I was shock to learn tat we need to go to polyclinic 1st to confirm we r pregnant and then receive the referral to kk hosp. Mind boggling with the half private half govt hosp or smtg. Referral to get subsidy by the way.

The basic needs are affordable.

The additional wants will have inflated prices.

And.one of the best way to keep cost low is having the grandma help take care too. I kinda feel sad when I hear 6 mth kids being put in daycare.

Cash flow is powerful.

LikeLike

Hi Rokawa,

Thanks for this! yes we are believers of the Rich Dad methodology too. 🙂

But the hard thing is – to get a portfolio to produce S$20,000 a year would require a lot more time! We are only getting S$2k – S$3k a year in dividend now haha. Of course the dilemma would be – do we drawdown from the portfolio? ideally not. Or do we set aside a baby fund / RSP now and that will reduce the amount we contribute into our dividend generating portfolio. I guess there’s no right answer to this.

And yes i think the Mrs Budget parents will be happy to take care of our future kid! That will definitely help us save a bit of money too.

LikeLike

Thanks for sharing 🙂 Always a pleasure reading people’s personal updates!

LikeLike