Syfe, a roboadvisor in Singapore, recently released a study that looks at whether Singaporeans are ready for retirement.

Dubbed the Syfe Retirement Readiness Index, the study showed a few findings after polling about 1000+ Singaporeans across all age groups.

Here’s what they found:

- 60% of Singaporeans feel that they are not adequately prepared for retirement

- 69% of Singaporeans don’t think they can retire comfortably

- 50% save less than 20% of their income

- 40% of Singaporeans are significantly behind on retirement planning

- Women are slightly more retirement ready than men

- Nearly 30% of homeowners saved less than 10% of their salary

What caught our attention is actually the low savings rate for the 35 – 44 age bracket – also most likely to be new homeowners and young parents.

Seeing that this will be Mr and Mrs Budget’s profile in the next few years, this worried us a bit too.

According to the study, for the 35 – 44 years old, only 52% save more than 20% of their salary, and nearly 30% of homeowners saved less than 10% of their salary.

With this in mind, we tried to do a forecast on our future expenses and see how much do we need to spend, and then we can work backwards from there to see how much we need to earn, in order to have excess money to save up for our retirement.

For the forecast, we will be calculating based on a young couple, with one kid as well as a maid to help with household chores, living in a private condo.

Currently, Mrs Budget and I spend about S$700 for groceries and meals, and we order in quite a fair bit.

With a child and a maid, we forecast the groceries and meal to be around S$1000 a month. For the home utilities, we calculated in the home utilities, mobile bills as well as the internet bill.

We estimate the cost of a maid to be about S$800. Other assumptions: mortgage payment will be S$3000 a month, and we are contributing a monthly stipend to our parents.

Hence the rough estimated household cost is at S$7,400 a month.

And wow that’s a lot.

We tried to see if our estimation is too far off, hence we compared this projection with another young family’s expense. We found that the figure is not too far off.

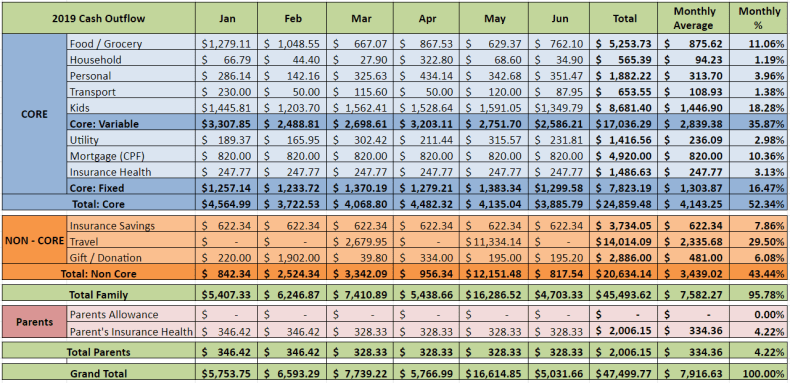

Here’s the real monthly expenses as shared by Dave and Kate:

From the above spending, you will see that the monthly average is S$7916.63 a month. Of course, they have two kids in the family so the expenses is slightly high.

So it will seem like the average household expenditure is around S$7000 – S$8000.

If we split that by two working adults, you will need to earn at least S$4,375 per person so that your take home pay is at least S$3500!

S$4375 per person can be quite high for some, and it is no wonder that young parents who are homeowners will struggle to save more than 10 or 20% of their salary every month. When the money comes in, all of it will have to be spent on household items, your child, your parents, and the hefty mortgage.

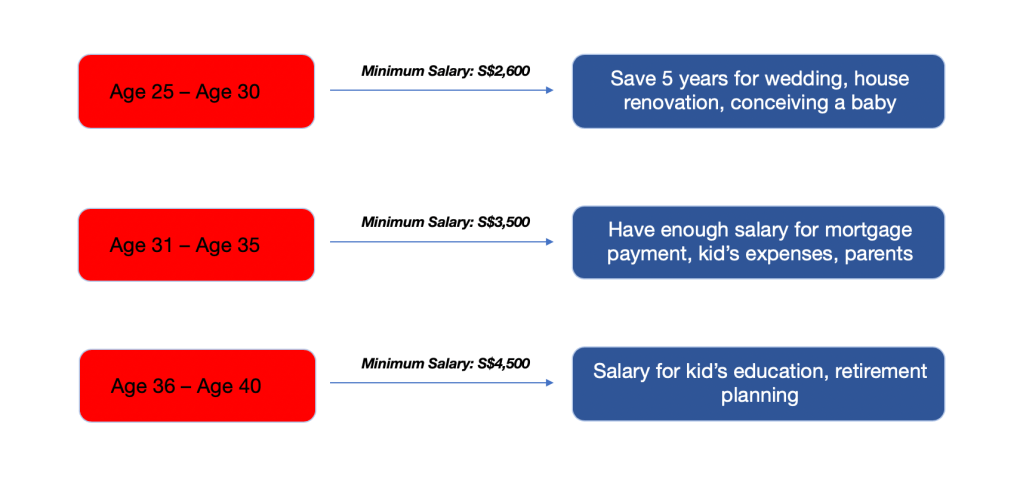

I’d imagine if a person is earning less than S$4,000 when he or she is older than 40 years old to feel as if he is living pay check to pay check. In my previous article, I have calculated that one have to earn at least S$2,600 a month before 30 years old.

Coupled with this new calculation, it seems like the ideal minimum salary range between 30 – 35 years old will have to be at least S$3,500 – S$4,500.

This way, he will be ready for all the mortgage and household expenses when he is 35 years old. This is also assuming the other partner has equal share in terms of household expenditure.

Also Read: At 30 Years Old, Your Monthly Salary Should Have Been S$2,600 For You To Feel Financially Secure.

Which is why prudent spending during your younger age is extremely important, and once you have this habit, you will bring it along with you even as you grow older.

It is also equally important to make sure that you increase your income every year, so that you can catch up with new expenses as we grow older.

For Mrs Budget and I, we will be using S$8,000 of monthly household expenses as a baseline to do a cash flow forecast for the next few years, and to see if our income can support that household expenses requirement.

Otherwise, we will have to make certain lifestyle adjustment to bring down the monthly household expenses. And it certainly looks that way now.

For our readers, do share with us your household expenditure so that we know if our figures are too far off. 🙂

Disclaimer: Figures above are not adjusted to inflation, and are only used as a general estimation. Real life expenditure varies from individual to individual.

Like our Facebook Page for more articles like this: Mr Mrs Budget

1. You don’t need to travel to work? That could be $2.60 returned x 2 pax = $5.20 a day x 22 working days = $114pm.

2. No travelling holidays? Even a simple Phuket trip for 3 pax would amount to $2k? That is only one trip per year. Another trip to Bali?

3. Other miscellaneous: wedding gifts, birthdays celebrations, hospital visits, wreaths, donations and CNY Ang pows….we are not living in an island!

4. Climate change- buying an air filter? Repair and replacement of furniture and appliances

5. Child schooling expenses- its more expensive in pre-school and childcare. A totler will quickly outgrow his clothings. New toys to sustain his interest all the time. Milk powder cost in Singapore is much higher than elsewhere.

6. Our perennially greedy Govt is imposing an increase in GST which our DPM explains is not based on needs but in anticipation of future need! Property tax even as owner-occupier is based on AV which is rent-based albeit a lower 4% if yours is in the lowest bracket. Assuming your condo unit rent fetches $3k pm, your Annual Value(AV)would be $36k, 4% of this would be $1440 for your annual property tax.

7. If your monthly expenditure is at this level of $7-8k, you are not likely to be income-tax exempt. Your taxman would be calling…

8. Only some pointers for teasers.

LikeLike

Seems to me the Dave and Kate expenses of 7k is due to 2k of travel, with 800 of mortgage. But your mortgage itself is already 3k. Mean they could save if they don spend on travel, but yours are more difficult.

LikeLike

Yeah there are definitely unexpected expenses that will pop up. One can only prepare for them as much as we can. 🙂

LikeLike

I have 3 kids 14-18, staying hdb paying cash for instalment monthly. My expenditure for normal days without travel is around $11-12k per month. No car, no branded goods, eat outside $200 meal once a mth. Paying insurance for 5 person, kids tuition already near $7k per month.

LikeLike

Hi Dan!

Oh wow 11-12k monthly expenditure seems very high. I think the tuition expenses seem to be slightly overbudget! Can be quite taxing to the monthly cashflow.

LikeLike

Well the ideal salary that’s based on S$3,500 to S$4,500 seems an unreliable fixed amount..

There could be several potential possibilities to ask for more salary increment other than the two figurative salaries as stated in the article above.

To conclude, it’s for everyone’s benefit.

LikeLike

Additionally, it’s good to have more substantial and informative articles such as these so that the entire community as a whole can have freedom of speech based on what’s being presented at hand 🙂

LikeLike

i have 2 kids. Stay in a 5 room hdb. Husband work from home while wife have to travel to work. No car.

Monthly morgage combine husband and wife cpf OA – $1.2k (No cash outlay)

Maid – $700

Electricty,water, gas bill – $120

Groceries + food ( cook most of the time otherwise pack food from cofeeshops nearby) = $400 – $500 ( wife has lunch provided by company)

Mobile bill – $45 (husband can claim mobile bill from company)

Internet bill – $39.90

Conservancy – $70+

Monthly expenditure on misc items – $200 to $400

1 Kid childcare fees – $300 ( subsidized rate as Wife is in the industry with subsidized staff rate for private childcare) (2nd kid take care by maid)

Insurance only took hospitalisation plans which is like only $200+ cash outlay per person per year for both husband wife and 1 kid. Another younger kid do not have any insurance yet. So i guess $600+ per year total.

Total expenditure prolly about $3600 to to $3800 plus minus.

Every month save about $5000 to $6000 combine.

usually travel once or twice per year to Japan, Korea, Taiwan etc but since covid, all travel plans halted.

Still able to constantly save per month with no issues. Have alot of entertainment at home as well so dont really need to go out so often.

I guess not everyone is like the topic starter that needs so much expenses. Its all about individual lifestyle.

LikeLike