Few nights ago, Mrs Budget shared something which we thought we should pen our thoughts down.

So over the past few months, Mrs Budget has been cashing out the money payments received from the loans she backed through funding society, a peer to peer loan financing company.

If you are unfamiliar with funding society, basically you can go onto the platform, look at profiles of companies who are asking for loans, and decide if you want to loan and help the companies out.

As these companies are usually rejected by bank loans due to higher risk, the interest on these loans can go up to between 10 – 20%.

Both Mr and Mrs Budget has been putting a small amount of money backing SMEs in Singapore, probably about S$5,000 total each.

For Mrs Budget, she shared that during the past few weeks, she has seen a lot of loan defaults on Funding Society, and that her capital is now mostly turning into a loss position, with only small chance of recovery.

What it means is that, Mrs Budget will most likely lose up to S$3,000 from funding society due to a non recoverable loan default!

For Mr Budget, he is still quite fortunate as his loans are quite diversified across many companies,. With his loan exposure per company set at S$200 max per company, the default rate is still quite manageable.

However, since February, Mr Budget has already disabled the auto-invest function under Funding Society and is now only collecting all the disbursed loans.

What he also noticed is that, the defaulting companies are skyrocketing since he last checked! Hopefully there will be lesser defaulting and non recoverable loans.

We also saw similar reviews on Seedly where a lot of retail investors have been saying that they are now sitting on capital losses although they have been investing for a while now.

Most of the investors on Funding Societies shared the same situation: investing over 2 to 3 years, from net gain to now net loss.

And all of this started in the past few months.

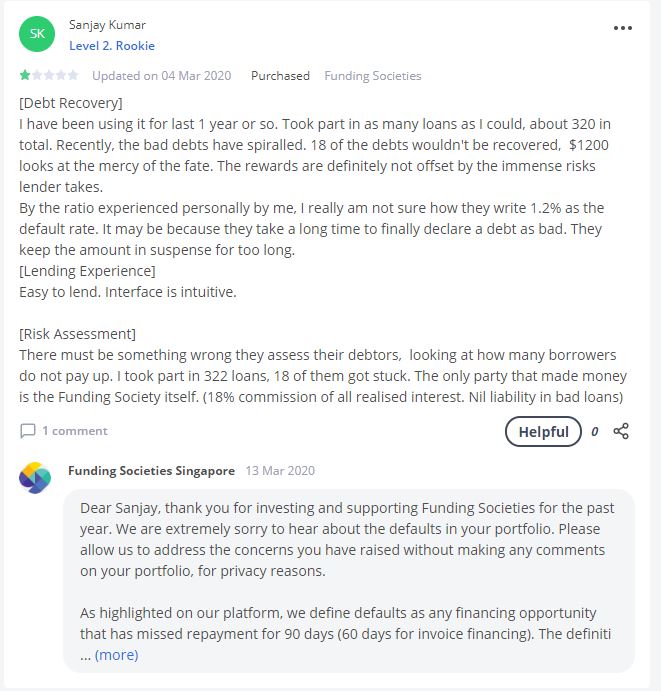

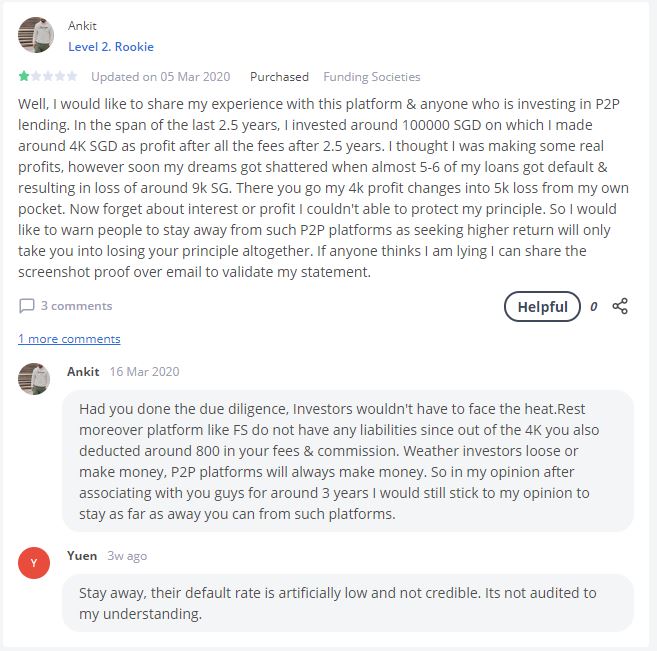

“Well, I would like to share my experience with this platform & anyone who is investing in P2P lending. In the span of the last 2.5 years, I invested around 100000 SGD on which I made around 4K SGD as profit after all the fees after 2.5 years. I thought I was making some real profits, however soon my dreams got shattered when almost 5-6 of my loans got default & resulting in loss of around 9k SG. There you go my 4k profit changes into 5k loss from my own pocket. Now forget about interest or profit I couldn’t able to protect my principle.”

To be fair, I don’t think its entirely Funding Societies’ problem. When times are good and when people earned up to 10% a year in the early days, no one complains. And now when companies start to belly up, then people complain.

Increasingly, I think more of these businesses are going to face more problems with cash flow, which will lead to loan defaults, and closure of businesses. Closure of businesses will then lead to unemployment, and then leading to individual cash flow problems.

This gives an early indication of the state of businesses in Singapore, and I think we are going to hear more from mainstream news soon.

Funding Societies or P2P loans are secondary market which provides liquidity for businesses – and with default rates ballooning up, this is yet another clear sign and indication that things will get worse.

For investors thinking of investing in high risk investment vehicles, this is definitely not a good time right now. For the amount of risk for platforms like Funding Societies, they will probably need to return 20-40%, as compared to a 3.35% – 23.87% return on investment based on 2019 figures.

Also Read: Our Thoughts On The Very Irrational Market Behaviour

Like our Facebook Page for more articles like this: Mr Mrs Budget

This is a good topic to write about, especially in times likes these. I didn’t even consider the impact of Covid-19 to investors in P2P lending platforms that provide financing primarily to Singapore SMEs. Which have been badly affected by the circuit breaker measures and hence the higher default rates. Thanks for highlighting!

LikeLike

Thanks Finance Smiths! Yeah usually the cards will fall in the secondary markets first before coming to the primary markets.

LikeLike

So glad I got out of FS 2 years ago. I invested in 10 SMEs, and 2 defaulted. It was impossible to know who would default or not based on the provided factsheets. It really is just luck.

That said, it is not so much the fault of FS then the state of the economy now. People were warned at the start there could be defaults. At rates of 7% or more, it is considered a high-risk investment. Every single other high-risk investment out there has gone down too.

LikeLike

Hi FI35, hope that you’ve been well.

It’s highly unusual to have 2 defaults in the first 10 loans invested. We are sorry for that. Having said that, investing in just 10 notes is not enough from a diversification point of view. We have investors who signed up around the same time as you, experienced a few defaults but yet still have a positive portfolio via proper diversification currently. We would be more than happy to address any queries you may have surrounding this so do reach out to us with your registered email address at invest@fundingsocieties.com.

On the other points you’ve highlighted, the fact sheet is meant to be a factual representation of the issuer’s financial standing at the time of underwriting. Through that, we illustrate why we have decided to crowdfund them based on their past business performance and cash flow. It gives us a clear assessment of the strengths of the deal but will not be able to guarantee a non-default situation. You would understand that all lending institutions including banks have defaults and they cannot predict a clean repayment with certainty for every loan that they give out.

You are absolutely right that the external circumstances are not the most conducive at this point in time and hence we are focusing more on Property-backed investments and Guaranteed investments while also ensuring that we only fund the low to medium risk industries for other products. We’ve tightened our requirements to remain vigilant about who we crowdfund. For example, we only fund certain favoured industries. Ideally, they should be able to thrive well during these times so industries like cleaning and maintenance, healthcare and medical are some of the ones we target. There’s also added emphasis on the source of payment from the issuer as well.

7% returns may not be considered a high risk investment given the short term nature of our notes since the majority of them have tenor of less than 6 months. We use tenor, amount and pricing to mitigate risks arising out of these investments. It’s a fact that many investors have fairly healthy investment portfolios on our platform which is also corroborated through our platform default rate of 1.75%.

We hope that we have been able to address some of your concerns. Please do not hesitate to reach out to us for a more detailed discussion. Thank you.

LikeLike

Really appreciate for sharing your experience. I’m also a victim. I joined Funding society less than 6 months before I stop investing on this platform. My default rate is 10%+, and total loss is 40%. Initial money is 10k, I have 3k+ in default status at this moment. I tried to contact FS many times but the reply is very disappointing, FS rejects to take any actions to help their customers. I have quite a lot of experience with P2P since 2013 both in Singapore and China. There is only one default experience and the company helped me to recovery my loss. Funding society is the worst and I’m not going to give up my money.

if you need more information from my experience, I’m willing to share. contact me at chris.loh9292@gmail.com

LikeLike

Hi Chris and good day to you. We hope to be able to better address some of the points you’ve mentioned but were unable to find any investor with your email address chris.loh9292@gmail.com. Do start a live chat with us at https://fundingsocieties.com/ or email us at invest@fundingsocieties.com to discuss your concerns again.

It would also be very helpful if you could share with us the kind of action you are referring to and what were some of the questions you’ve asked us before? If it is recovery related, we may not always be able to recover from the defaults as is what happens with all lending financial institutions. Nonetheless, we’ve also had multiple successful recoveries in the last couple of years where not only have we recovered full principal but interest as well.

Our platform default rate is 1.75% which you can monitor on our website. Losing up to 40% of your capital in a span of 6 months is an extremely rare scenario and seems to suggest over exposure to a few issuers and not enough diversification. To illustrate the above point, here’s a simple numerical example to show that it is still possible to suffer defaults but have a net positive portfolio. Assuming that one made 100 x $50 investments and each have a 10% return. If 4 of these go into default, it’d be a $200 (4%) loss. The remaining investments would yield a return of $480 (10% x 96 x $50). Returns after defaults would be $280 and after the 18% service fees, the investor would still get $229.60.

We hope that we have been able to address some of your concerns. Feel free to reach out to us for further discussions. Thank you.

LikeLike

Hi, i have invested some monies into Funding Societies 2.5 years ago, with proper cash management into the p2p loans as a lender, by putting about 1% to 1.5% of my total investment per loan. To cut the story short, over more than hundreds of loans that i have participated as a lender, close to 12 loans defaulted, 1 loan unrecoverable and 11 loans are in process of recovery (for many months). And the potential lost is 10% even with all the interests gained by other loans thus far.

In short, i doubt Funding Societies (FS) is able to recover the monies for the lenders and have to move on and out of FS as I am not doing charity.

LikeLike