Earlier last week, after reading our post on the ideal minimum salary range and the thoughts on retirement, Syfe reached out to us to have a chat with us on our financials.

We subsequently agree and met up earlier today.

If you didn’t know, Syfe is a roboadvisor which adopts a hybrid model – there is the automated monthly investment portion and it is complemented with a human financial advisor.

From a methodology point of view, compared to the other roboadvisors in Singapore, Syfe believes that your investment should be more about managing its risk and if that is properly defined, you are able to see what your potential returns (and subsequently your portfolio allocation) are based on your acceptable risk.

This approach is in line with Mr Budget’s view towards investment – the first step to investing is to know what is your risk profile.

For Mr Budget, I am a rather impatient guy, and has a relatively high risk profile.

Hence when I first dabbled into investment, my first stocks that I bought were all US stocks. US stocks is probably one of the investment product with the highest risk (daily fluctuation of 1-5%). With an understanding that my investment journey will be at least 10 to 20 years old, I am more focused on building my capital now.

US stocks also fits me the best because it can provide a decent capital gain in a short period of time (although this can go both ways). I can also accept the higher risk that comes with this.

For other products like ETFs, local REITS et cetera, you can only see the return in 5-10years for the compounding interest to kick in.

So this forms the fundamentals of my investment strategy:

- For the first 2-3 years, aim for capital gain via higher risk instruments

- With the capital gain, invest them into relatively safer instruments such as REITs and subsequently fixed income or bonds.

- Rinse and repeat, and at year 5 – 10, I should have built up a strong portfolio of REITs as well as holding on to some of my US stocks which hopefully have become multi baggers by now

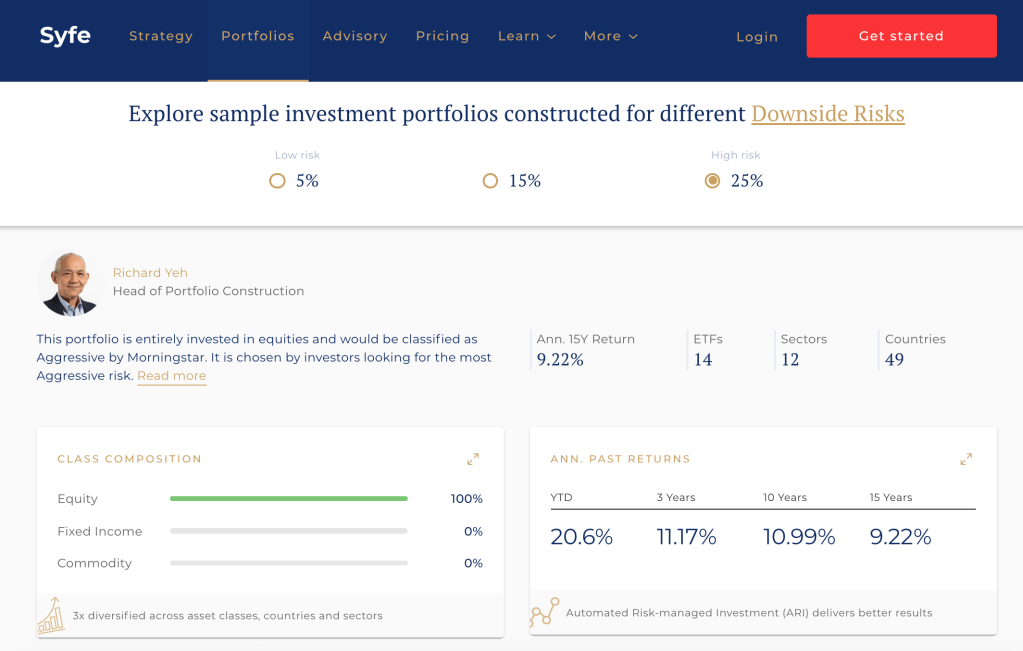

For Syfe, the process is largely similar, you identify your risk profile, and then you will be allocated a recommended portfolio based on the maximum drawdown you are able to take.

So for example, taking the self assessment test on Syfe, my risk profile will be the highest, and I am recommended the high risk portfolio with a potential drawdown of 25%.

This portfolio has a 100% equity allocation.

One of the pointers brought up by Syfe’s head of investments was that, for DIY investors (like us), how often do we beat the index?

More often than not, we can’t, because there are just too much information out there, and that we might miss out on some opportunities because we are caught up with other aspects of life.

And that is true, if I look at the returns I generated for my portfolio over the past few years, I have not beaten the index at all. So perhaps, our portfolio has been lacking a roboadvisor component which serves as a “professional managed” portion of our overall portfolio.

For a while now, we have been looking to try out roboadvisors, and do monthly regular investments into these platforms and let professionals manage a small portion of our portfolio for us.

Who knows, with the addition of roboadvisors in our portfolio, our overall portfolio might enjoy higher returns.

The outreach by Syfe is timely since this has been in our mind for a while now, and we will most probably be starting a regular investment into Syfe.

This post is not sponsored, and nor was there at any point did Syfe ask us to help promote the brand, but here are some personal thoughts which I like about Syfe:

- Relatively low fees (0.4% – 0.65%) + 0.15% ETF fees, with no withdrawal fees, no trading fees and no entry or exit charges

- The investment methodology is in line with my belief

- Investment team is definitely more experience than I am

- Aggressive portfolio allocation is investment in not just companies that I am similarly following (US high growth equities), but also in other industries I am not familiar in: utilities, consumers, energy etc. Would love to have some exposure to these areas which I am not familiar in.

- Access to financial advisors to periodically check in on any gaps that we may have in our financial planning process

To me, the last question I ask myself is, what is the risk for this other than market risk, which I am also exposed to. The biggest risk is that Syfe closes down, and that we will lose all of our capital. But that is minimised by the fact that they are regulated by MAS, and that they have several high profile backers. Hopefully that doesn’t happen.

So for Mr and Mrs Budget, we will most probably start to park a monthly amount to Syfe and use that as our emergency + retirement hybrid fund.

When we start doing that, we will be tracking the monthly investment gain from the portfolio and share it with you guys. 🙂For now, Mr Budget will have to go back to number crunching mode to see how much we can invest and what will the impact be towards our financials projection before committing an amount.

If you are looking to sign up for Syfe, here’s a referral code for you: SRP6X8B8Y

If this referral code, you can get $50 when you invest S$10,000.

Are you investing in any roboadvisors?

Like our Facebook Page for more articles like this: Mr Mrs Budget

Hi. Not a regular here but just wanted to comment on some things for your consideration.

1) I don’t think Syfe markets itself as active management. You can google to find out how many active managers (amateur or professional) actually beat the market. The trend in passive investing is because of that.

2) There are other Robos out there. Why Syfe? StashAway also seems to define it’s portfolios by risk level. AutoWealth also has competitive fees.

3) Syfe invests in US ETFs. You pay dividend withholding tax for that up to the tune of 30%. Did you know that? Granted StashAway and AutoWealth have this same problem, but on the other hand, Robos like Endowus and MoneyOwl do not. Have you considered them?

Just curious about your thinking. =)

Thanks for sharing your thoughts.

LikeLike

Hi Oken,

Thanks for sharing your thought process too!

1) Not really looking for active managers. Syfe mostly invest in baskets of ETFs which id think they had professionally looked at them and picked them. They might actively rebalance these ETFs allocation based on the risk profiles. 🙂

2) You are right. I think it’s hard to choose the BEST roboadvisor. Syfe, Stashaway and Autowealth probably has a lot of similarity as you rightfully pointed out. For stashaway, i have an inactive account, and i just logged in to see where they invest in for my allocated risk factor: they invest across a wide range of geography, and US is only a small portion only. Plus they invest in gov bonds (30% of my portfolio) I also didnt like Stashaway that much as it doesnt allow me to adjust my risk factor (i wanted max risk). I thought that was restrictive to me because for me, I have my other non-risky investment to balance out my overall portfolio, and wanted maximum risk for my roboadvisor, but stashaway made that decision for me and assigned me a lower risk portfolio. Autowealth if im not mistaken, has a minimum investment. For Syfe, it’s portfolio allocation is very heavy on US equity allocation, which fits what I am looking for.

I think ultimately, you choose what makes you comfortable. It’s like choosing a cinema to watch a movie, all of them allows you to achieve your goal of watching a movie (get automated exposure to markets that you are not tracking, managed by professionals), but you see which cinema you are comfortable in. 🙂

3) I have heard about Moneyowl too. For the withholding tax, yes we are paying that for our US holdings too. But for Syfe, i felt like they made an effort to reach out, and we felt somewhat comfortable with them. Perhaps in picking Syfe there was some qualitative factor in the works where everything fell in place.

I think it’s really hard to pick the best roboadvisor, and perhaps 10 years down the road only can we see the performance of the various robos. If Syfe can return me an annual return of 10+% as indicated in its sample 25% drawdown risk portfolio, I will actually be very very happy with the results.

If not, i can only curse and swear haha and hopefully the other robos will not overperform that much. Also, i can fall back to see if my own managed portfolio performs better than Syfe’s professionally managed portfolio. After all, for Syfe, it will only be meant as my emergency fund + makes up a small portion of my retirement fund. 🙂

– Mr Budget

LikeLike

Hi Mr Budget,

I am a DIY investor like you and like you I prefer the US stock market even though prices are all time high currently. I love the US stock market because of the vast amount of ETF offerings.

1. I would rather just buy plain vanilla total market ETFs rather than use the roboadvisors: example VTI for us stocks, VT for global. Expense ratios are like 9 basis points. Like what you mentioned in your article, I don’t aim to beat the market.

2. I used to have stashaway but I felt they were too active in a sense because they have like 15+ ETFs plus they switched my portfolio in mid 2019 during the trade war because their system detected a recession (yield curve also inverted then). But it never came and the us stock market soared. As a result, my portfolio would have become too conservative and missed out the year end rally of 2019.

3. I currently use moneyowl because they give me access to dimensional funds which provide some tilt towards small cap and value. 100% equity portfolio. So maximum risk. Endowus also provided access to dimensional funds which is inaccessible to diy investors like us.

Please do check my blog: http://www.fattysfinance.com

I am new to this so I would appreciate any tips to grow it.

LikeLike

Hi Fatty Finance! Thanks for your comments. I guess there are no right and wrong answers just one that suits each individuals. A lot of people have been talking about moneyowl and endowus. I should probably look at them!

Congrats on the new blog! Have checked them out. Keep up the sharing 🙂

LikeLike