So the market dived another 8-10% or so yesterday.

Every retail investors is probably mass selling and taking profit off their positions now.

There were reports that trading firms are overwhelmed and true enough, when I log into Vickers, I couldn’t even connect to my account. This truly is a once is a decade / life time event.

I wouldn’t lie, when the market crashed, it has been emotionally testing – its painful to refresh my app to see the market prices.

So earlier today, I went ahead to do a quick number crunching to see the impact of a further 20% drop of my equities towards my retirement / S$1M goal projection.

Here’s a look at the previous projection with the following assumptions:

- US Equity – Monthly Contribution with an overall portfolio growth rate of 8%

- SG Equity – Monthly Contribution with an overall portfolio growth rate of 5%

- Syfe – Monthly DCA with an overall portfolio growth rate of 5%

- Annual EPF and CPF contribution at current level.

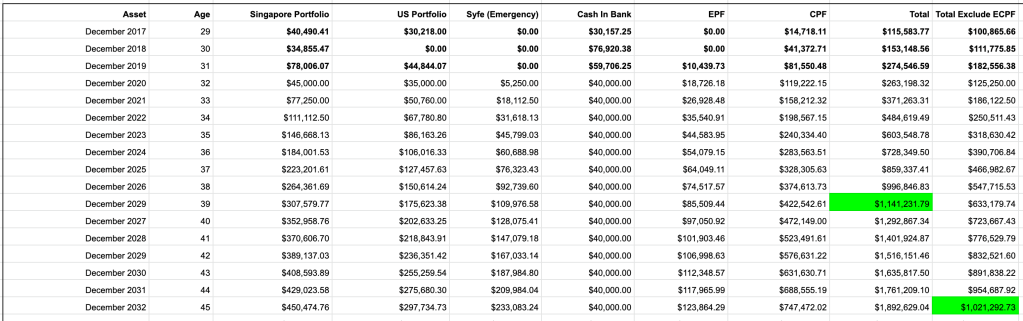

According to the earlier projection, excluding our properties and mortgage, we should

- Hit a net worth (Equities, Cash, CPF) of S$1M at end 37 years old, or in December 2025.

- Hit a liquid net worth (Equities, Cash) of S$1M at 42 years old, December 2029.

However, as the market plunged this week, we now have to add new numbers into our projection model.

What we did was:

- Update our projected 2020 numbers by entering current portfolio number

- Add a further 20% drawdown to all our current equities position

- Stop our US, SG, and Syfe Investment contribution for this year

Based on the 3 new parameters, here’s the updated impact towards the 1M goal.

Based on the table, just by adding a further 20% drawdown on our equity position and stopping our investment this year, our S$1M net worth (ex property and mortgage) goal is pushed back from December 2025 37 years old to December 2026 38 Years old.

If we exclude CPF (liquid net worth), the impact is even bigger: our S$1M goal is pushed back from December 2029 42 Years old to December 2032 45 years old, a good 3 years goal push back!

Which means now, if everything stay constant, I have to work for another 3 years just because the market crashed.

Of course, while this is bad news, we also acknowledge that the growth rate once the market recovers will hopefully be able to counteract the current decline in our portfolio and hence move our current target back on track.

This exercise paints a good picture for us to see the impact of the current equity drawdown on our portfolio, and to really reassess our portfolio resilience.

Currently our cash level is the highest it has been since the past 2 years as we manage to sell some stocks before the second wave of crash. Hence we will be accumulating our war chest and deploy them when situation show more signs of stabilisation.

I feel like there will be a further 20-30% drawdown in the market because we have yet to see the domino effect of the global virus situation – ie the housing and credit crisis.

So things will probably get worse, as we also have a significant exposure in properties.

You can also read about our horrible experience not being able to sell our stock via DBS Vickers: Earlier Today I Experienced Every Investor’s Worst Nightmare – Unable To Sell My Stock

Like our Facebook Page for more articles like this: Mr Mrs Budget