Recently Mr Budget received a comment from a reader (thank you! We love reading them!) commenting on the CPF scheme.

Ronald shared his views that I should do a calculation on the CPF Life annuity scheme to see if it is a fair deal before committing so much into CPF, after all CPF contribution is a one way street – once you put in the money, you can only see it more than 25 years later.

That prompted Mr Budget to do some digging.

Many in the financial space will be familiar with Kyith’s work from Investment Moats, and we are also big fans of his.

Kyith always use data to support his articles, and when we dug deeper into his archive of works, we found that he calculated the returns of CPF Life, which saved us the trouble of doing the calculation ourselves.

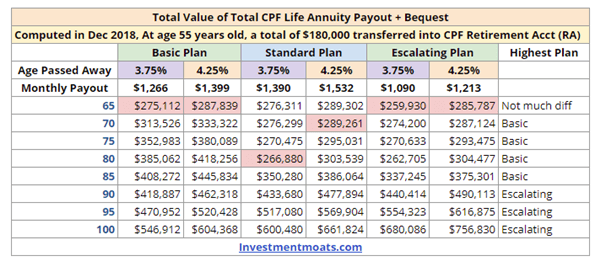

In case you are unfamiliar with the CPF Life scheme, at age 55, CPF will automatically create a new Retirement Account (RA) for you. The source of the RA account come from both your OA and SA account. For us, we foresee that we will be able to hit the full retirement sum, which is at S$181,000 now.

Here’s the internal rate of return Kyith simulated based on the following parameter: Computed in December 2018, at age 55, a total of S$180,000 is transferred to the RA account.

As Kyith rightfully pointed out, the IRR and amount disbursed changed according to the age you pass away.

For Mr Budget, I foresee I will be able to live until 65 – 70 years old, hence the IRR for the basic plan will be between 3.97% to 4.33%, with me getting back between S$275,112 to S$313,526 from the S$180,000 CPF retirement scheme.

Of course, there are a lot of moving parts in calculating the IRR and amount received as the government will raise the basic retirement sum over time and they might also adjust the payout amount, but at this point we can only hope that Singapore has our best interest in mind, and that we can only plan based on current data.

So the question is, are we happy with the returns? I’d say we are quite happy with the results as it is quite rare for us to be able to find a guaranteed annuity giving this rate of return, especially since we expect our risk profile when we are older to be significantly lower than what we have today.

Of course, knowing the payout only paints part of the picture.

The reason why we actively contribute to the CPF account is also we see this as part of a forced savings so that we can really see compound interest in the works when we are older.

Here’s Mr Budget’s projected CPF with the following parameters: constant CPF contribution from employment as well as annual S$7,000 RSTU scheme, at an annual interest of 3.5% (instead of 4%).

| Year | Age | Start of Year CPF | CPF Contribution | CPF Interest | End of Year CPF |

| 2017 | 29 | $0.00 | $14,370.65 | $347.46 | $14,718.11 |

| 2018 | 30 | $14,718.11 | $25,624.74 | $1,029.86 | $41,372.71 |

| 2019 | 31 | $41,372.71 | $36,730.00 | $3,063.91 | $81,550.48 |

| 2020 | 32 | $81,550.48 | $33,640.00 | $4,031.67 | $119,222.15 |

| 2021 | 33 | $119,222.15 | $33,640.00 | $5,350.18 | $158,212.32 |

| 2022 | 34 | $158,212.32 | $33,640.00 | $6,714.83 | $198,567.15 |

| 2023 | 35 | $198,567.15 | $33,640.00 | $8,127.25 | $240,334.40 |

| 2024 | 36 | $240,334.40 | $33,640.00 | $9,589.10 | $283,563.51 |

| 2025 | 37 | $283,563.51 | $33,640.00 | $11,102.12 | $328,305.63 |

| 2026 | 38 | $328,305.63 | $33,640.00 | $12,668.10 | $374,613.73 |

| 2027 | 39 | $374,613.73 | $33,640.00 | $14,288.88 | $422,542.61 |

| 2028 | 40 | $422,542.61 | $33,640.00 | $15,966.39 | $472,149.00 |

| 2029 | 41 | $472,149.00 | $33,640.00 | $17,702.61 | $523,491.61 |

| 2030 | 42 | $523,491.61 | $33,640.00 | $19,499.61 | $576,631.22 |

| 2031 | 43 | $576,631.22 | $33,640.00 | $21,359.49 | $631,630.71 |

| 2032 | 44 | $631,630.71 | $33,640.00 | $23,284.47 | $688,555.19 |

| 2033 | 45 | $688,555.19 | $33,640.00 | $25,276.83 | $747,472.02 |

| 2034 | 46 | $747,472.02 | $33,640.00 | $27,338.92 | $808,450.94 |

| 2035 | 47 | $808,450.94 | $33,640.00 | $29,473.18 | $871,564.12 |

| 2036 | 48 | $871,564.12 | $33,640.00 | $31,682.14 | $936,886.27 |

| 2037 | 49 | $936,886.27 | $33,640.00 | $33,968.42 | $1,004,494.69 |

| 2038 | 50 | $1,004,494.69 | $33,640.00 | $36,334.71 | $1,074,469.40 |

| 2039 | 51 | $1,074,469.40 | $33,640.00 | $38,783.83 | $1,146,893.23 |

| 2040 | 52 | $1,146,893.23 | $33,640.00 | $41,318.66 | $1,221,851.89 |

| 2041 | 53 | $1,221,851.89 | $33,640.00 | $43,942.22 | $1,299,434.11 |

| 2042 | 54 | $1,299,434.11 | $33,640.00 | $46,657.59 | $1,379,731.70 |

| 2043 | 55 | $1,379,731.70 | $33,640.00 | $49,468.01 | $1,462,839.71 |

If all things stay constant, Mr Budget should be able to hit S$1,000,000 in his CPF by age 49. That is really quite a lot, and from the table, you will see that every year, the interest received is getting higher and higher, and we earn the magical interest on interest.

To be honest, we have yet to enjoy the benefits of compound interest especially in our current bank account because we are always moving our cash around. Our cash in bank will also be depleted every time we have a new milestone in life.

Hence CPF in a way is really our “forced savings” portion of our portfolio, for us to really see the effects of compound interest. There is probably no other ways we can clearly see this manifested in our lives other than CPF because we tend to move our funds around, and that’s always the case for Mr Budget.

By age 55, after setting aside the basic retirement sum, Mr Budget can also withdraw the rest out for usage.

We confirmed that we can withdraw the rest of our CPF based on the CPF withdrawal Q&A on the CPF website.

Of course, this is the idealistic projection because there are many unforeseen things that could happen:

- Government might change certain rules with regards to CPF withdrawals or interest rates.

- Mr Budget might lose his job or have a pay cut

- Mr Budget may need money for his child expenses, hence the annual contribution will be reduced by S$7,000

- Mr Budget passes on before 65 years old.

If Mr Budget really passes on before 65 years old, then the S$180,000 would not be worth it. By then, money wouldnt matter anymore to me haha.

So to Mr Budget, the main reason for the annual CPF top up is basically leveraging the CPF to get an annual 4% interest rate so that we can see a compound growth over the next decade and we can enjoy the fruits in the future. The annuity portion of CPF life is really just a small reason why we actively contribute to CPF.

And hopefully the government don’t introduce big changes to the CPF scheme over the next 30 years!

Also one last note, this post is not to show off the CPF amount, because the truth is, the same compound interest applies to everyone, and if most people chart their CPF projection, they will most probably get similar graphs.

It’s to share our thinking behind why we contribute regularly and to visualize (in numbers) compound interest in the works. This is also not any investment advise as Mr and Mrs Budget is just 2 regular working PMET trying to make sense of our financials and to plan for the future. 🙂

Like our Facebook Page for more articles like this: Mr Mrs Budget

An average salary worker who buys a BTO & doesn’t play the property upgrading game can easily hit their cohort’s FRS amount by 55 yrs old. Without additional contribution to CPF. Really! Of course this assumes he doesn’t get stuck in a low-wage job or unable to achieve average salary due to accident, handicap, critical illness etc.

Whatever that is above the FRS or BRS, you can take out in 1 lump sum at 55, or leave inside CPF as a high-yield savings account, or to take out only bit by bit. Up to you.

As for the IRR or returns or yields of CPF Life … take it from any insurance or financial industry insider … there’s NO commercial annuity on the market that can match CPF Life returns based on lifetime tenure.

CPF Life overnight basically destroyed the annuity business for S’pore’s insurers. Now only those with too-much-money-already-have-bungalow-and-lambo will buy commercial annuities.

LikeLike

Hello!

You are absolutely right. 🙂 We also think that its hard to find any other annuity in the market similar to CPF Life. And we are also on the same page with regards to property upgrading – i think its very hard to always change properties because the next upgraded property will erode away any gains from your first property and comes at a higher pice / ie higher mortgage payment which translate to higher CPF OA deduction.

LikeLike

so most importantly is to invest in your health earlier on so that one can live longer and leverage on the cpf life scheme

LikeLiked by 1 person

Hi Redfield,

Yes haha may we all live long and prosper. But actually it can be hard to live a healthy lifestyle because we just get caught up in our day to day. But that shouldnt be an excuse to not exercise often. 🙂

Happy new year to you!

LikeLike

I had turned 55y in yr 2019 n reached the required 176k. This year 2010 i learned that my earned interests cannot be withdrawn. I had read many bloggers m articles n strangely this point was not mentioned.

LikeLike

Earned interest in RA cannot be withdrawn. Only earned interest in SA & OA.

If your MA has hit BHS limit, then earned interest from MA can also be withdrawn.

If you have money in both SA & OA after 55, then better to withdraw 11 months earned interest in Dec. If wait till Jan, the full year interests will be credited into the respective SA & OA accounts — you won’t be able to withdraw the OA interest amount without having to withdraw all your SA first.

CPF has algorithm for sequence of withdrawal.

LikeLike

There are some nuance to it. if you are not able to withdraw, perhaps you could check with the cpf folks why it cannot be withdrawn. Like what Sinkie say, interest from different pots of money has different status.

LikeLike

Thanks for mentioning my stuff! The math is that you will have something like this. So now the further question is how does this 1 mil fit into your overall plan.

LikeLike

The table is based on the Full retirement amount being used to buy annuity. In reality, only half of retirement sum is used at age 55. The other half is only used at age 55 to buy another annuity. Hence the IRR will be different.

LikeLike

Hi, I thought a more conservative approach would be calculating the special account growth instead of a combination of OA, MA and SA (I assume your calculation is based on entire contribution to 3 accounts). This is because OA will be used for housing (usually) and MA for medical. Do note that RSTU stops when SA hits FRS as well.

LikeLike

Hi Evans! That’s a fair point and thanks for pointing that out! Will do an update to the projection. 🙂

LikeLike

i have just one thing to say. I hope Mr and Mrs Budget being PMETs themselves….don’t lose their jobs to foreign talents (through no fault of both sides of course) *winks*

Losing their job would severely throw a spanner in the works of this ‘blue sky’ scenario article. Gotta admire your positivity 🙂 thumbs up!/

LikeLike

Haha we hope so too! Hope for the best but plan for the worst! 🙂

LikeLike